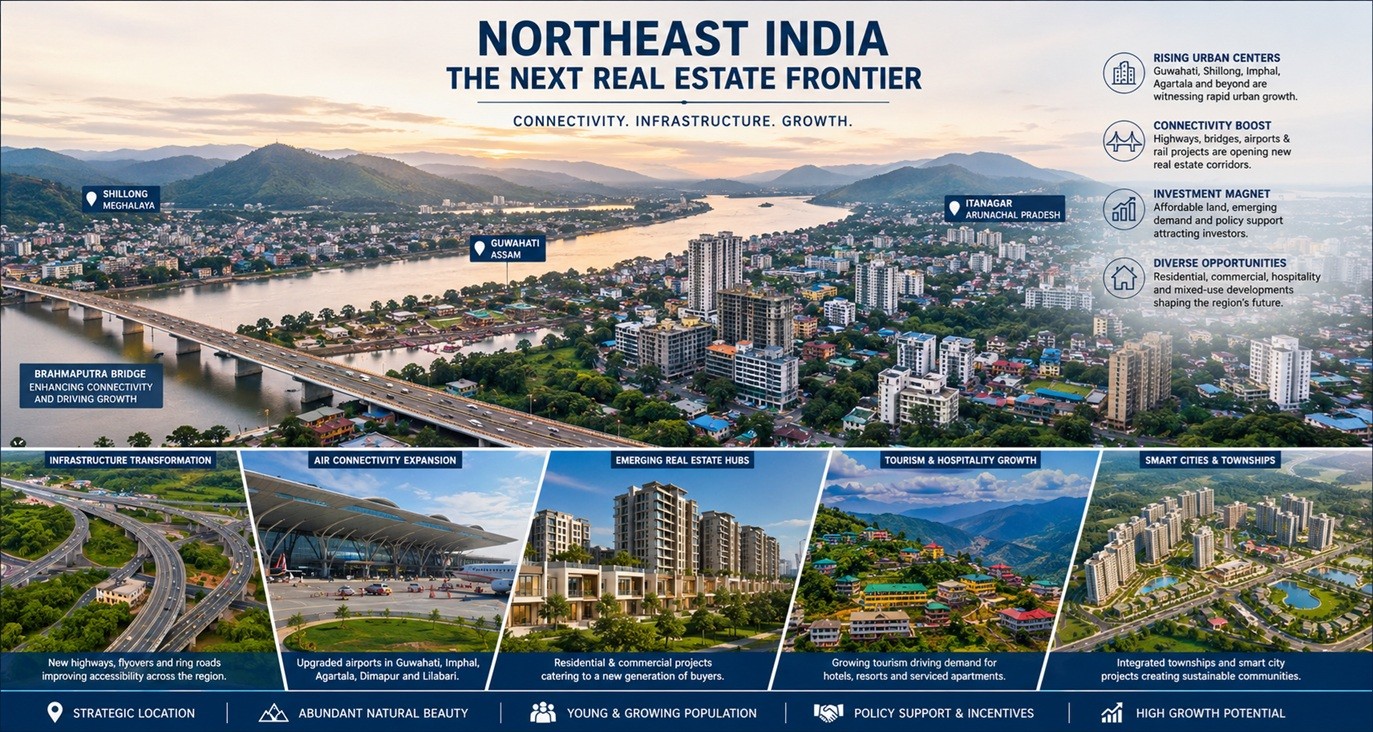

The Seven sisters, once viewed as the quiet edge of India’s commercial map, are now sprouting as the nerve centre of an emerging regional real estate Supercycle. India’s real estate story has always followed infrastructure, but what is unfolding in Northeast India, that represents something fundamentally different. The Northeast is no longer just a tourism gateway, rather it is rapidly evolving into a high-stakes industrial and commercial corridor, which is going to redefine India’s property landscape by 2035. The Knight Frank’s Q1 2026 data indicates a cooling in traditional metros like Pune, Mumbai, Bangalore and NCR; sales across these metros fell about 4% year-on-year, launches continue to out space absorption for the 14th consecutive quarter and sold inventory now substantially sits above 519,000 units.

Northeast India is now running at the same playbook at scale as traditional metros in terms of sustained property bloom. Beginning with Guwahati’s 93-km Ring Road, which unlocks entirely new development corridors in Azara, Baihata and Narengi. The Baghdogra airport expansion plan has also fueled a 10-million-passenger capacity. Furthermore, the JLL’s research corroborates what developers have already sensed on the ground: Guwahati’s office stock is expected to move up to 80% from 2 million sq ft in 2024 to 3.6 million sq ft by 2027. Now, where office demand goes, residential demand inevitably follows. Moreover, IHCL has already moved into Dibrugarh with a Ginger hotel and signed into Sikkim and Arunachal Pradesh. Ambuja Neotia and Apeejay are actively stitching joint ventures into North Bengal and Siliguri. These are not leisure plays. They are institutional signals that the commercial and residential markets behind them are about to follow.

Here is what most traditional estate commentary misses entirely: Northeast India is not just a frontier market in the romantic, speculative sense. While traditional real estate hubs are grappling with price appreciation testing affordability, the Northeast on the other hand, is benefiting from massive capital infusions. The Advantage Assam 2.0 Summit in early 2025 witnessed investments commitments exceeding ₹2.5 lakh crore, with Reliance, Adani, Vedanta and Tata collectively pledging into the region. When four of India's most data-driven conglomerates place concurrent bets on the same geography in a single summit, that is not optimism. That is the thesis– and the real estate market is only beginning to price it in. The Northeast is not replicating metro growth patterns, it’s pioneering a post-saturation model where affordability, infrastructure catalysts and land monetization innovations converge. In about a decade, it is expected that Northeast India’s story will be spiraling from a single city or quarter to a rolling regionalisation of India’s economic growth.