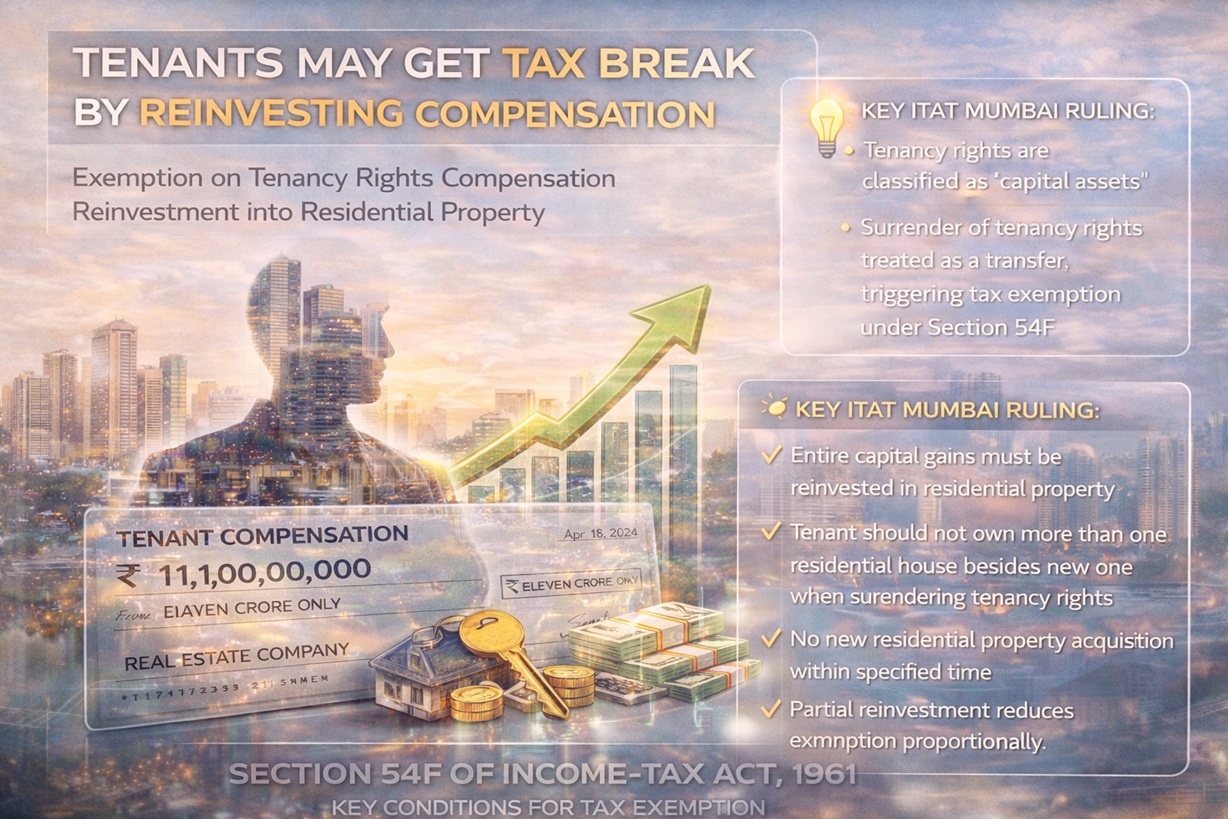

Tenants who surrender their tenancy rights may find themselves in a favorable tax situation if they reinvest the compensation received into residential property. A pivotal ruling from the Income Tax Appellate Tribunal (ITAT) in Mumbai clarified that tenancy rights are classified as capital assets. This classification is crucial because, upon surrendering these rights, the tenant experiences a transfer, making the compensation eligible for a tax exemption under Section 54F of the Income-tax Act, 1961, provided certain criteria are met.

In a notable case, a tenant received compensation valued at Rs 11 crore for surrendering his tenancy rights to an apartment in Mumbai. Initially faced with a tax notice from the Income Tax Department, the tenant successfully contested the ruling in ITAT Mumbai, resulting in the exemption from income tax on the received compensation. This case underscores the importance of understanding how tenancy rights are treated under tax law, especially in relation to capital gains.

According to experts like Chartered Accountant Suresh Surana, tenancy rights fall under the definition of a 'capital asset' as outlined in Section 2(14) of the Income-tax Act. When these rights are relinquished, the transaction is considered a 'transfer' under Section 2(47). Consequently, any monetary or non-monetary compensation received by the tenant is subject to taxation as capital gains, specifically under Section 45, rather than as income from other sources. This distinction is critical for tenants looking to navigate the complexities of tax liability when surrendering tenancy rights.

To benefit from the tax exemption outlined in Section 54F, tenants must adhere to specific conditions. The exemption applies if the net proceeds from the transfer of any long-term capital asset, excluding residential houses, are reinvested in purchasing or constructing a new residential property in India. Notably, the tenant must not own more than one residential house (aside from the new purchase) at the time of the transfer and must refrain from acquiring or constructing another residential property within the stipulated timeframe. If the entire net consideration is reinvested, the capital gains will be fully exempt; if not, the exemption will be proportional, calculated according to the formula laid out in Section 54F(1). Thus, tenants surrendering their rights can potentially enjoy significant tax benefits, provided they comply with the legal stipulations governing such transactions.