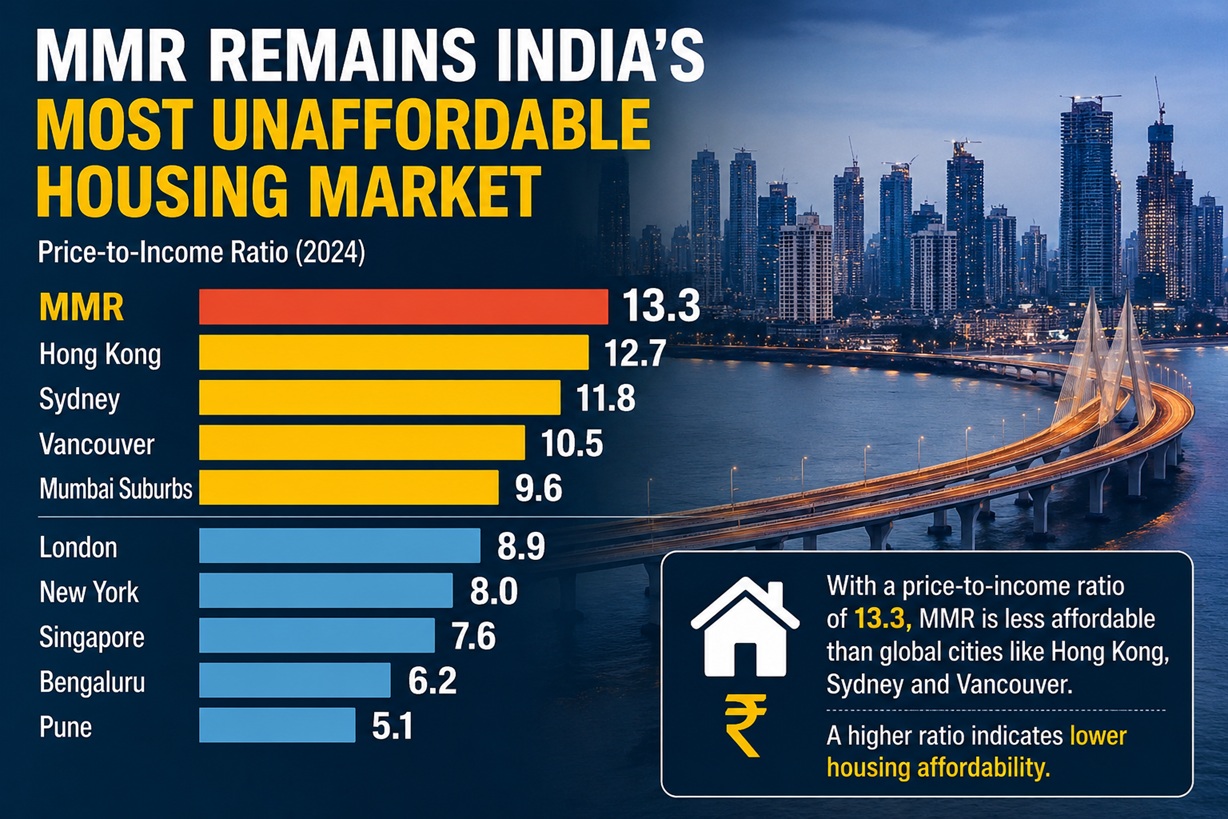

The Mumbai Metropolitan Region (MMR) has been identified as the least affordable residential market in India, according to the latest Affordability Index released by Knight Frank. The report highlights that homebuyers in the MMR are required to allocate approximately 69% of their household income to cover equated monthly installments (EMIs) on home loans. This situation persists despite the recent trend of lower home loan interest rates, which have provided some relief to buyers in other major cities across the nation during the first half of 2026. In contrast, the MMR, along with the National Capital Region (NCR), remains one of the only markets where the affordability ratio exceeds the generally accepted threshold of 50%. This statistic underlines the significant financial strain faced by potential homeowners in this region.

The Knight Frank Affordability Index assesses the percentage of household income needed to meet monthly EMIs for a standard housing unit, with a measurement above 50% indicating a lack of affordability. In the case of the MMR, the affordability level has remained consistent at 69% for the first half of 2026, mirroring the figures from the previous year. While this marks an improvement from the 77% recorded in both 2016 and 2019, MMR continues to be characterized as the most expensive housing market in India. The report attributes the stable affordability levels to the cumulative effects of the Reserve Bank of India's monetary easing, which has led to a reduction in borrowing costs. Though lower interest rates have helped mitigate some of the rising property prices, they have not sufficiently improved the affordability situation in Mumbai.

Despite the easing of home loan rates, the persistent rise in residential property prices in Mumbai poses a significant barrier for many buyers. Reports indicate that even with the benefits of reduced borrowing costs, residents still find themselves dedicating over two-thirds of their monthly income to EMIs, a situation that is particularly challenging when compared to other major Indian cities. Knight Frank notes that while affordability had seen a gradual improvement between 2016 and 2021, the trajectory shifted in 2022 when the Reserve Bank of India increased the repo rate to combat inflationary pressures. Since early 2023, a period of rate stability followed by monetary easing has contributed to a stabilization of affordability levels, yet rising property prices continue to offset these gains.

The Monetary Policy Committee's decision to maintain the repo rate at 5.25% during its recent meetings reflects ongoing concerns regarding geopolitical tensions and other economic uncertainties. This decision is likely to sustain stable financing conditions in the foreseeable future. As highlighted by Shishir Baijal, Chairman and Managing Director of Knight Frank India, these findings underscore the pressing need for policies aimed at enhancing housing affordability in the MMR. As the market continues to grapple with these challenges, the burden on homebuyers remains a critical issue that requires concerted attention from stakeholders across the real estate sector.