The dream of owning a home remains a significant aspiration for many individuals in India. Home loans play a crucial role in making this dream attainable, and public sector banks (PSUs) such as the State Bank of India (SBI) and Central Bank of India are instrumental in offering affordable interest rates. As of 2026, the Indian banking landscape is characterized by competitive home loan rates, largely influenced by the Reserve Bank of India's (RBI) recent rate cuts in 2025. With the RBI's Monetary Policy Committee (MPC) meeting approaching in April, stakeholders are closely monitoring potential changes in repo rates, which could directly impact home loan interest rates across both public and private sector banks.

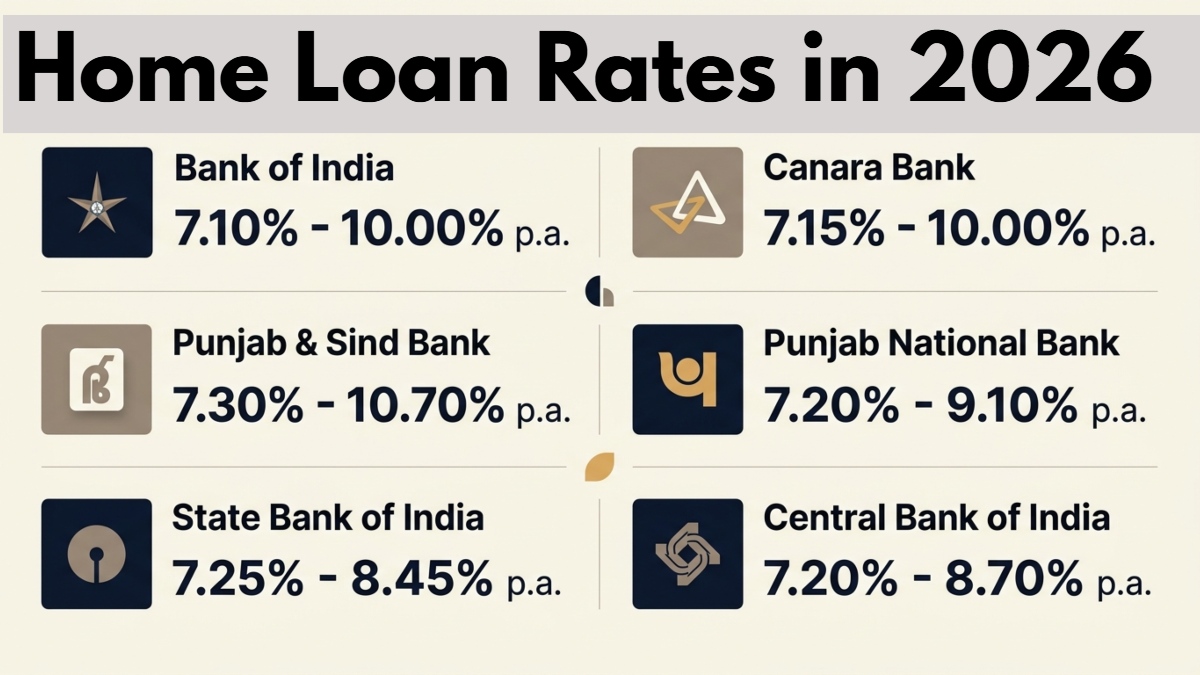

Currently, the SBI, recognized as the largest public sector bank in India, offers home loan interest rates ranging from 7.25% to 8.45%. The actual interest rate applicable to individual applicants may vary based on factors such as credit score, property location, and overall financial profile. Similarly, Punjab National Bank (PNB) presents home loan interest rates between 7.2% and 9.1% per annum. While these rates are relatively lower compared to some competitors, the final rate is contingent upon the applicant's CIBIL score and other relevant details.

Additionally, Canara Bank provides competitive home loan rates, ranging from 7.15% to 10.00% per annum. This positions Canara Bank as a strong contender among its peers, enhancing accessibility for potential homeowners. Furthermore, the Central Bank of India offers home loan rates within the range of 7.2% to 8.7%, along with attractive options for various categories of home loans, including loans for third or fourth houses, Cent Home Loan Double Plus, and Cent Grih Lakshmi Loan. These diverse offerings cater to a wide array of customer needs, thereby promoting homeownership across different segments of the population.

As the housing market continues to evolve, prospective homebuyers are encouraged to stay informed about the latest developments in interest rates and consider how their financial health may influence their loan terms. The ongoing discussions surrounding the RBI's repo rate will be pivotal in shaping the lending landscape, and individuals are advised to consult with financial advisors to navigate their options effectively. By understanding the nuances of home loan interest rates and leveraging the offerings from public sector banks, buyers can make informed decisions that align with their financial goals.