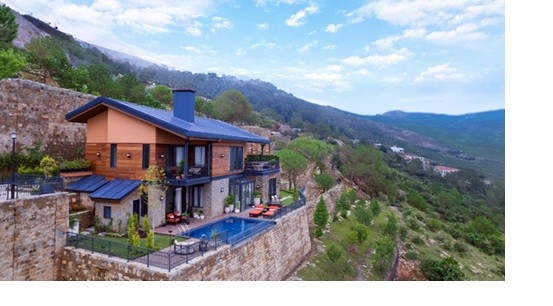

Over decades, nostalgia has served as the foundation for the Indian ambition of acquiring a second residence- a quiet bungalow in a serene and off-beat location intended for retirement. However, in recent years, India’s mainstream residential landscape has undergone a fundamental shift. While the metropolitan markets grapple with rising unsolid inventory, Holiday homes are quietly emerging as double income-generating assets. Holiday homes- once branded as the idea for rich men’s indulgence, are now being reimagined as a new investment frontier which is swiftly gaining its momentum. Places like Goa, Lonavala, Alibaug, Rishikesh and Coorg are no longer seen as weekend escapades, instead, these regions are recognized as the primary catalysts for a structural evolution where refined living intersects with robust yield-based financial strategies.

What accelerates this transition is the convergence of forces which ceased to coexist even a few decades ago. To begin, the widespread adoption of hybrid work models has liberated a new generation from the constraints of metropolitan living. This cultural pivot has effectively transformed the traditional second home into a primary residence for extended durations. Moreover, the surge in domestic tourism has also played an important role. Reports show that Goa as a tourism hub alone has witnessed over 10.4 million tourist arrivals since 2024 marking a 21% jump year-on-year. Also, The Knight Frank Q1 2026 report further confirms an ongoing volatility in the market. Residential sales have substantially moderated by 4% year-on-year to 84,827 units, with the gap between launches and absorption widening to over 10,000 units- the highest since Q1 2023. Compared to the conventional 2-3% yields from standard residential assets in Tier-1 hubs like Mumbai, Bengaluru, or the NCR, holiday homes in tourism hotspots have provided generously about 5-9% annual return through short-term rental platforms. Consequently, the vacation rental market has witnessed a rather aggressive trajectory, expanding from USD 330 million in 2023 to over USD 500 million by 2025, projecting a robust 23% CAGR. Prominent investors are recognising the current consolidation in tier-1 markets is not a crisis but a mere realignment. What differentiates the vacation properties from the traditional residential investments are the dual value propositions: substantial capital growth within the perimeters of trending tourism corridors aligned with immediate rental revenue generation. As validated in the Knight Frank’s note, India is stepping into a “more calibrated phase” with its real estate market.

Holiday homes in India’s most sought-after travel destinations are no more just a backup plan. They are rapidly becoming the main event—one where investors are gradually transcending beyond the residential landscape to a far more experience driven yield-focused portfolios.